Humans love to compete. This desire to win is so strong that our history is filled with examples:

- Cain and Abel

- Countless Wars

- Olympics

Today, this competition is still rampant. Countries, businesses, and individuals all compete with each other to win a prize whether that’s recognition or land or profits.

In the business context, competition mean more people fighting for the same pie. This makes it harder for businesses because their share of this pie gets smaller and smaller.

But what if there was a way to not compete at all, yet still win? What if there was a way to make your competition irrelevant?

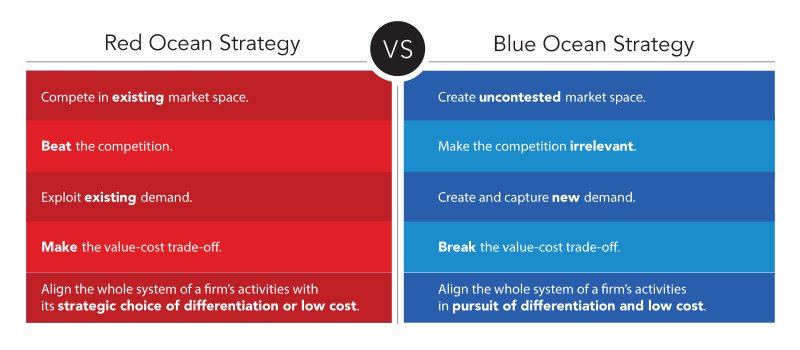

Enter: the Blue Ocean Strategy.

At its core, the Blue Ocean strategy is all about creating new, uncontested market space that bring profitable growth instead of competing with one another. If you haven’t read this book and you own a business or plan to start one, grab your copy now.

And as brands become more similar, people increasingly base purchase choices on price—Blue Ocean Strategy

The sentence above in the book summarizes the need to create blue oceans. The more you compete, the less there is for everyone. If you want to make your competition irrelevant, stop competing. Here’s one way to do that:

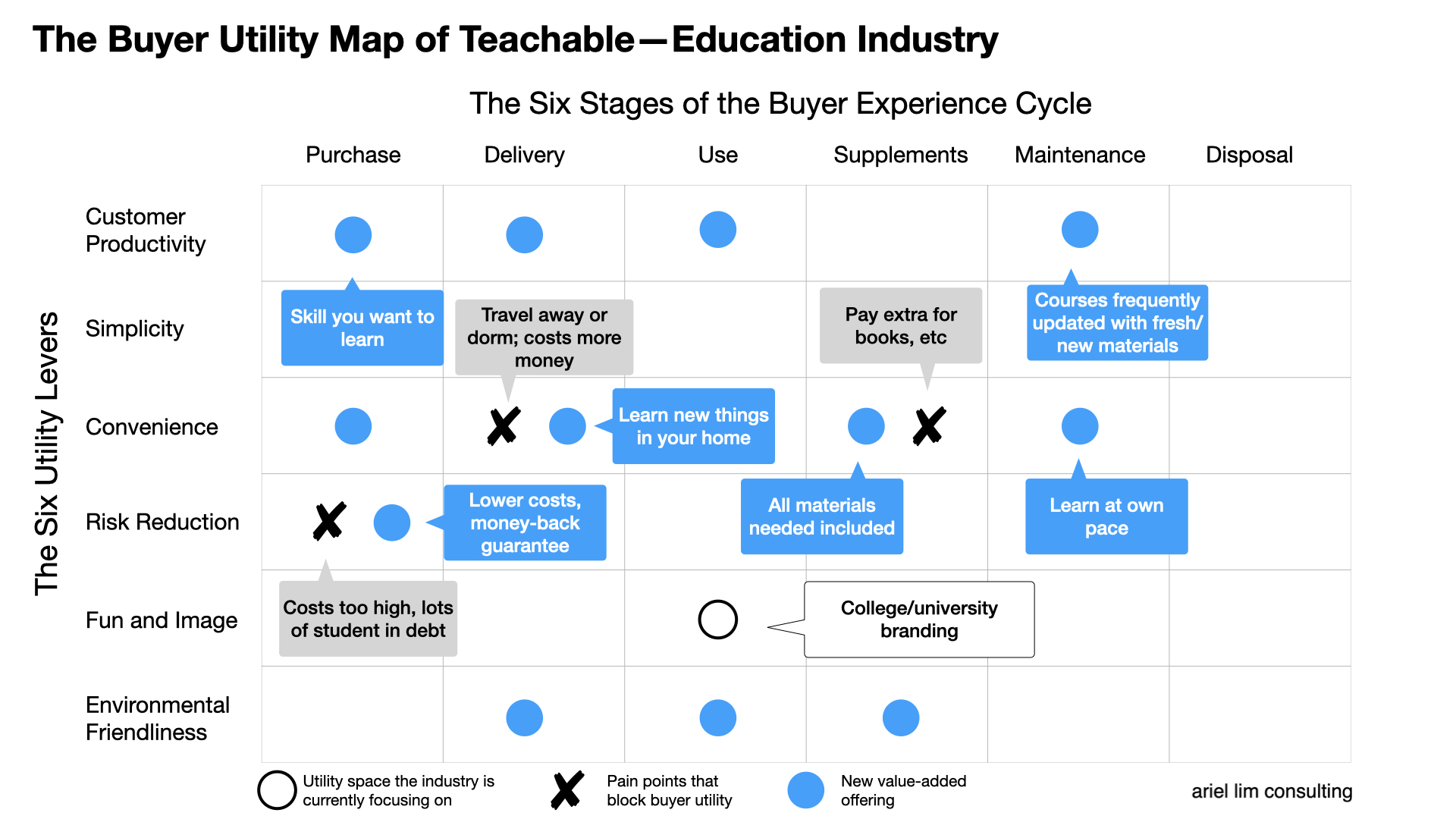

Find Hidden Opportunities in Your Industry Using the Buyer Utility Map

The buyer utility map is one of the tools of the Blue Ocean Strategy you need to understand if you want to stop competing. It allows you to visually see where the entire industry is focusing on during the entire buyer’s journey across six utility levers.

Here’s how the buyer utility map would look like for Teachable or other online learning platforms. It looks at the education industry as a whole, map out the factors they are focusing on, and see all the gaps everyone else is ignoring.

This tool is a starting point for your new offering. Because you can visually see the gaps, you can brainstorm ways how you can fill those in. Now, you have the potential for a blue ocean offering.

Validate Your New Business Idea Using the Stair Step Method

Once you identified your offer, whether that’s a new product line or a new business entirely, you don’t allocate money immediately, even if you have some to spare. Use the stair step validation method.

Here’s how it looks like:

- Ask for interest

- Get their commitment

- Go for the sale

The main point of the stair step validation is to reduce your risk of failure. Uncertainty is a given in any business. There are various ways you can do this and the stair step validation method is one of them.

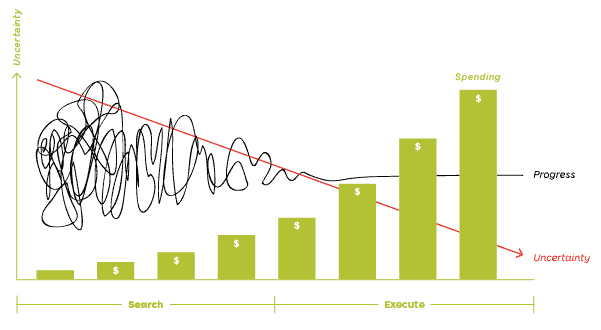

Take, for example, this image from Strategyzer. At the early stages, there is so much risk and uncertainty that you should spend your time validating your assumptions instead of spending money. As uncertainty goes down, that’s the time you invest heavily.

The stair step validation works in the same way. By asking for interest in the idea, you are reducing your uncertainty by getting feedback from other people. This allows you to refine your offering further.

As you progress, the next step will be getting commitment to support the idea. In essence, you are generating leads (or potential customers) even before developing anything. This will naturally involve more discussions internally and externally to refine your new offering.

After refining your idea and getting commitment, it’s time take the ultimate validation test: ask for the sale. If people are willing to give you their hard earned money even if the product or service or business has not yet been launched/developed, that’s a great sign that it’s a winning idea.

Double-Down on What’s Working

After identifying hidden opportunities in your industry and validating your assumptions, you’re now left with a potential winner. The only thing that’s left is execution, or to use a better term, iterative implementation.

You don’t separate planning from execution. The moment you think these two activities don’t go hand-in-hand, you’ll start to lose.

If you go back to the steps above, there is some level of planning involved but implementation is key. You get feedback, then improve. You can’t do that by spending all your time creating spreadsheets and reports.

Over to You

Starting a business is easy. Growing and making it successful is the hard part. If you’re like most businesses, you’re probably trying to find ways to get new customers and grow your revenues or your market share by outdoing your competitors. This leads everyone to compete on prices, which results to a smaller piece of the pie.

If you want to avoid this cycle, stop competing. Take the time to find hidden opportunities in your industry. Test your assumptions one by one. As your risk and uncertainty goes down, you can start pouring more money to your winning idea. From then on, it’s all about execution.

Netflix saw this opportunity, tested their assumptions, found out what works and what doesn’t, invested on those that work, and grew to where they are today.

They made their competitor irrelevant by not competing with them. Today, Blockbuster is no more. Copycats are playing catchup. But the fact remains you can succeed in business without competing.

Is there a new business offering that you’d like to launch? Or are you going to compete every day for the rest of your life for the market?

Either way, I’d love to hear your thoughts.